Dive Brief:

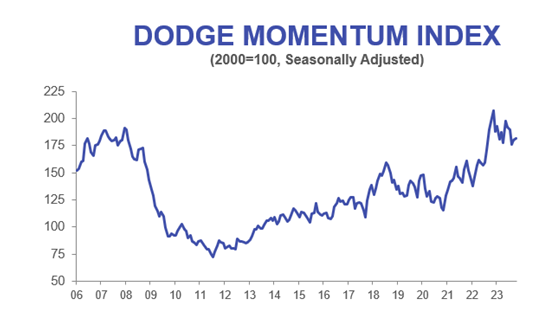

- The Dodge Momentum Index, a benchmark that measures nonresidential building planning, inched up 1% in October driven largely by warehouse activity, according to the Dodge Construction Network. It’s the second consecutive month of positive gains.

- September’s report reversed six months of contractions. This month’s sequential gain suggests that the index, which peaked in December 2022 and typically leads actual construction spending by 12 months, continued to build on its positive direction.

- “Heightened momentum in warehouse planning activity supported the commercial side of the index this month, while muted education planning activity slowed the institutional portion,” said Sarah Martin, associate director of forecasting for Dodge Construction Network. “Overall levels of planning activity remain robust and will support construction spending over the next 12 to 18 months.”

Dive Insight:

Martin said last month that lingering high interest rates, supply chain snarls and tighter lending standards are likely to continue to weigh on the commercial segment, such as office, retail and warehouse projects.

So, while improvements in warehouse planning pushed the overall commercial component to rise 2% in October, concerns remain around the segment’s outlook. Year over year, the DMI for the commercial segment remains down 14%, according to Dodge.

On the institutional side, which includes education, life sciences and healthcare projects, the segment also posted a drop in planning, falling 1.4% in October, according to Dodge. Nevertheless, the sector as a whole has been largely resistant thus far to market headwinds, said Martin. Year over year, the institutional segment remains up 7%, according to the report.

“Month-to-month movement in the index can be volatile, but 2023 trends continue to show an overall decrease in commercial projects, offset by more institutional projects entering the planning queue,” said Martin. “Commercial planning has been generally in decline since its peak last November but has begun to stabilize in recent months.”

ABI continues to drop

Meanwhile, the Architectural Billings Index, which also provides a leading indicator for upcoming construction work that’s nine to 12 months out, continued to deteriorate, according to the most recent data from the American Institute of Architects. The ABI score of 44.8 is the lowest score reported since December 2020 — during the height of the pandemic — and indicates that the share of firms reporting declining billings has significantly increased.

“Owners want to build, but inflation is wreaking havoc with financial proformas and forcing cost cutting measures on many commercial projects so that they can proceed,” according to a 12-person firm in the Northeast referenced in the AIA report, with both commercial and institutional specialization.

According to Dodge, a total of 21 projects valued at $100 million or more entered the planning stages in October. The largest commercial projects included:

- The $215 Google data center in Kansas City, Missouri.

- The $180 million Mauna Kea Beach Hotel in Waimea, Hawaii.

The largest institutional projects to enter planning included:

- The $400 million Grand Sierra Resort Arena in Reno, Nevada.

- The $267 million renovation to Keller Auditorium in Portland, Oregon.