Dive Transient:

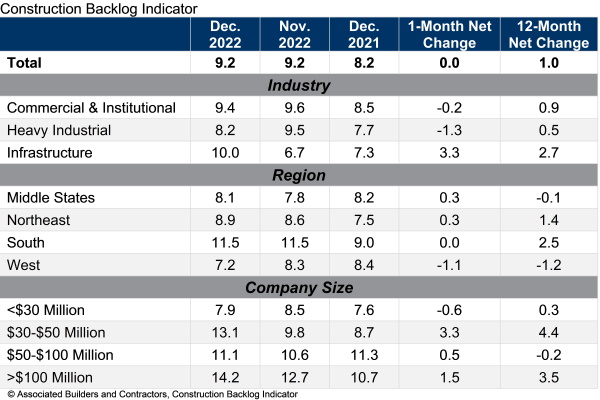

- Building backlog remained unchanged in December at 9.2 months, in accordance with Related Builders and Contractors. The numbers present a cushion for the sector towards a possible recession, however the group’s economist stated motive for warning stays, as larger prices for capital stymied some initiatives.

- ABC’s Building Backlog Indicator reached its highest degree in November because the second quarter of 2019, as contractors with beneath $30 million in income landed new jobs quicker than anticipated. That prime water mark was matched once more in December.

- “Contractors enter the brand new 12 months with loads of optimism,” stated Anirban Basu, ABC chief economist, within the launch, however added “contractors might quickly present extra concern. Anecdotal proof means that financing business actual property initiatives is harder.”

Dive Perception:

The robust backlog studying signifies the development trade continues to fend off any recessionary considerations for this 12 months, Basu stated. “Even when the financial system had been to enter recession this 12 months, contractors would probably be insulated from vital hurt.”

Meaning for now, building execs are emphasizing the constructive.

“Fairly than fixate on the opportunity of a recession, many contractors stay centered on progress, with expectations for rising gross sales and staffing ranges over the following half 12 months,” stated Basu. “Even the studying on revenue margins elevated this month, maybe reflecting an improved provide chain.”

However whereas the report suggests optimism in 2023, contractors’ outlook might quickly flip extra pessimistic. Financing business actual property initiatives has develop into more difficult, largely resulting from recession predictions, stated Basu.

“The final improve in the price of capital has additionally jeopardized many initiatives,” stated Basu. “Sure contractors [are] noticing a rise in postponements.”

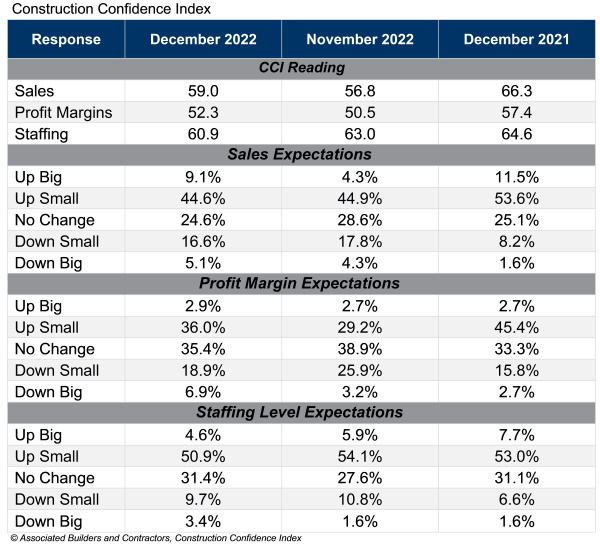

ABC’s studying for revenue margins and gross sales jumped in December, whereas the studying for staffing ranges decreased. Whereas all three readings stay above the edge of fifty, indicating expectations for progress over the following six months, they had been considerably decrease than year-ago ranges.