Dive Brief:

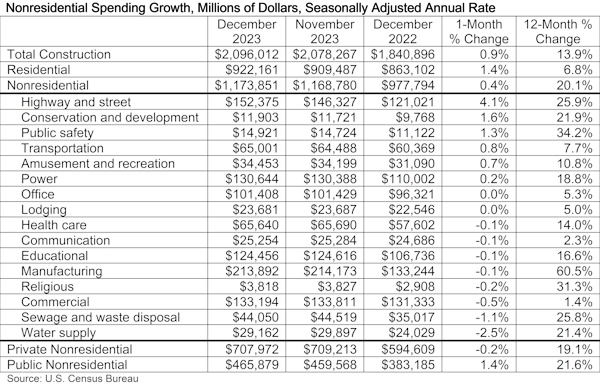

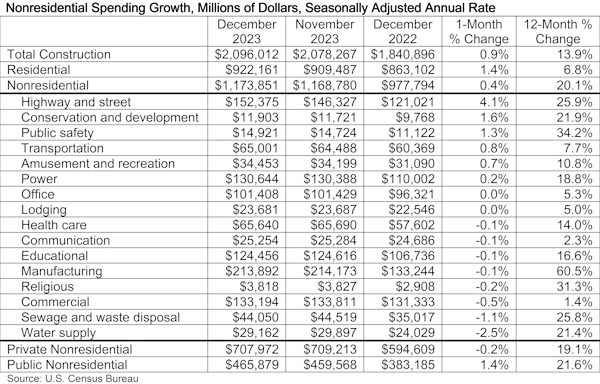

- Nonresidential construction spending rebounded 0.4% in December to a seasonally adjusted annual rate of $1.17 trillion, according to Associated Builders and Contractors’ analysis of U.S. Census Bureau data.

- But the overall rise masks a tale of two markets, one where publicly funded nonresidential activity jumped 1.4%, while spending on private projects dropped 0.2%.

- “That decrease in private activity was offset by surging activity in the highway and street category, which along with other publicly financed segments will retain momentum in the coming months as infrastructure investments are finally put in place,” said Anirban Basu, ABC chief economist.

Dive Insight:

After a revision flipped November’s 0.1% drop back to positive, December’s jump now marks the 19th consecutive month of growth, largely due to infrastructure and manufacturing activity, Basu said, noting big gains for spending overall last year.

“Nonresidential construction spending finished 2023 up more than 20% and will carry ample momentum in 2024,” said Basu in the release. “While much of that strength is due to surging investment in new manufacturing structures, roughly half of the 16 nonresidential subsegments saw spending increases by 20% or more in 2023.”

Notably, highway and street projects increased 4.1% in December, leading all subsectors in nonresidential construction.

Even with strong momentum and overall market strength, though, lingering high interest rates, coupled with labor shortages and regulatory delays, could still impact the positive trajectory of construction spending, according to the Associated General Contractors of America.

That’s particularly concerning for private-sector construction demand, according to the AGC report.

“Despite overall strong market conditions, there are a number of reasons to be cautious about how 2024 will play out for the construction industry,” said AGC CEO Stephen Sandherr in the report. Issues he listed include a need for more education and training for workers, as well as expedited permitting reviews.

Nevertheless, Basu noted that surge in activity within the highway and street category offset the decrease in private activity. He added the infrastructure sector, along with other publicly financed segments, will retain momentum in the coming months as investments are put in place.

AGC Chief Economist Ken Simonson also echoed a cautious sentiment but expressed optimism about sector growth as a whole.

“Construction spending rose across the board in 2023 despite higher interest costs, shortages of workers and delays in awarding federal money for infrastructure,” said Simonson. “These challenges remain in early 2024 but the industry is poised for further growth overall.”